Business Term Loans: A Comprehensive Guide for Small Business Owners

High Amounts, Stable Rates, Long Terms — Your Complete Guide to Business Term Loans

ENGLISH

6/26/20255 min read

Term loans are one of the most common financing options available to small businesses in the United States. They offer a lump sum of capital that must be repaid over a set period of time with interest—often used for capital expenditures, expansion plans, equipment purchases, and other long-term business investments.

In this guide, EZ Capital will explain what a business term loan is, its advantages and disadvantages, loan types, who qualifies, and how term loans compare to SBA loans. We aim to make this complex topic simple and accessible so that every business owner can make informed financing decisions.

1.What is a Term Loan?

A business term loan is a type of financing where a business borrows a fixed amount upfront and repays it in installments over a predetermined period—typically at a fixed interest rate. Terms can range from one year to five, ten, or even twenty-five years. Repayments are made periodically (usually on a monthly basis) until the full principal and interest are paid off.

In many ways, a term loan is similar to a car loan or mortgage, except it’s used for business purposes. Term loans can be obtained from traditional banks, credit unions, or online lenders. Funds can be used for a wide range of business purposes, including expansion, equipment purchases, inventory, marketing, debt refinancing, or real estate acquisition. Because term loans typically offer fixed interest rates and predictable monthly payments, they are often one of the more affordable financing options available to small businesses with numerous benefits.

Tip: Fixed Interest Rate vs. Floating Interest Rate

A fixed interest rate remains constant throughout the loan term, ensuring that your interest rate and monthly payments are locked in. This predictability simplifies budgeting, as your repayment amounts won't change, even if market interest rates rise.

In contrast, a floating interest rate (also known as a variable interest rate) fluctuates periodically based on changes in a benchmark index, such as the prime rate or the Secured Overnight Financing Rate (SOFR). This means your interest payments can increase or decrease over time, depending on the market.

Example: If you borrow $100,000 at a fixed annual interest rate of 5%, you'll pay $5,000 in interest each year, regardless of market fluctuations. While for floating interest rate, if you borrow $100,000 with an initial annual interest rate of 4%, and the benchmark rate rises to 6%, your annual interest payment would increase to $6,000. Conversely, if the benchmark rate falls to 3%, your annual interest payment would decrease to $3,000.

2.Advantages and Disadvantages of Term Loans

✅ Advantages

High Loan Amounts & Long Repayment Terms

Business term loans can range from tens of thousands to several million dollars. Repayment terms are flexible—typically from one to ten years. For commercial real estate loans, terms can be as long as 25 years.

Relatively Low Interest Rates

Compared to high-interest financing options like business credit cards or merchant cash advances (MCA), term loans generally offer lower interest rates. Most term loans are fixed-rate, helping businesses manage consistent monthly payments and minimize exposure to interest rate fluctuations.

Fast Online Approval Options

In addition to banks, many online lenders can approve and disburse funds within a few business days. This speed is especially helpful for businesses with urgent needs, such as time-sensitive purchases or seasonal inventory.

Flexible Use of Funds

Term loan proceeds can be used for a wide variety of business purposes: expanding operations, purchasing equipment, launching marketing campaigns, restocking inventory, consolidating debt, and more. Unlike certain loan programs (e.g., SBA 504), term loans typically do not impose strict use limitations, making them ideal for diversified small business operations.

❌ Disadvantages

May Require Collateral or a Personal Guarantee

Larger loan amounts often require collateral, such as commercial property or equipment. Most lenders will also require a personal guarantee from the business owner—meaning if the business cannot repay, the owner is personally liable.

Less Flexibility in Repayment

Once the loan is funded, fixed monthly payments are required regardless of how your business is performing. In periods of slow revenue or market downturns, these fixed obligations may strain cash flow and disrupt daily operations.

Risk of Default and Asset Loss

Late or missed payments can result in penalties, damage to your credit score, legal action, or even asset seizure if the loan is secured by collateral.

3.Types of Term Loans

Term loan programs are commonly categorized by the length of repayment period:

(1) Short-Term Loans

Term: Typically 3–18 months

Loan Amount: $5,000 to $250,000

Features: Fast approval, suitable for urgent short-term needs like emergency repairs or bridging cash flow gaps

Interest Rate: Relatively high

(2) Medium-Term Loans

Term: Usually 1–3 years

Loan Amount: $25,000 to $500,000

Features: Ideal for moderate investments such as equipment purchases or business expansion

Interest Rate: Moderate, lower than short-term loans

(3) Long-Term Loans

Term: Typically 3–25 years

Loan Amount: $100,000 to several million dollars, depending on business size and creditworthiness

Features: Suitable for major investments and long-term financing like real estate acquisition or mergers

Interest Rate: Lower, but requires stronger financials and often collateral

4.Suitable Applicants and Eligibility Criteria

Term loans are best suited for established businesses with a strong financial track record:

Time in Business: At least 1 year of operating history (2+ years preferred by banks). Online lenders may accept 6–12 months.

Revenue: Minimum annual revenue of $100,000 is common. Financial statements or bank statements may be required to prove consistent cash flow.

Credit Score: A personal credit score of at least 550 is typically required. A strong credit history will improve your chances of approval and reduce your interest rate.

Collateral / Personal Guarantee: For larger loans, lenders may require business assets as collateral or ask the owner to personally guarantee repayment. If the business defaults, the owner's personal assets may be at risk.

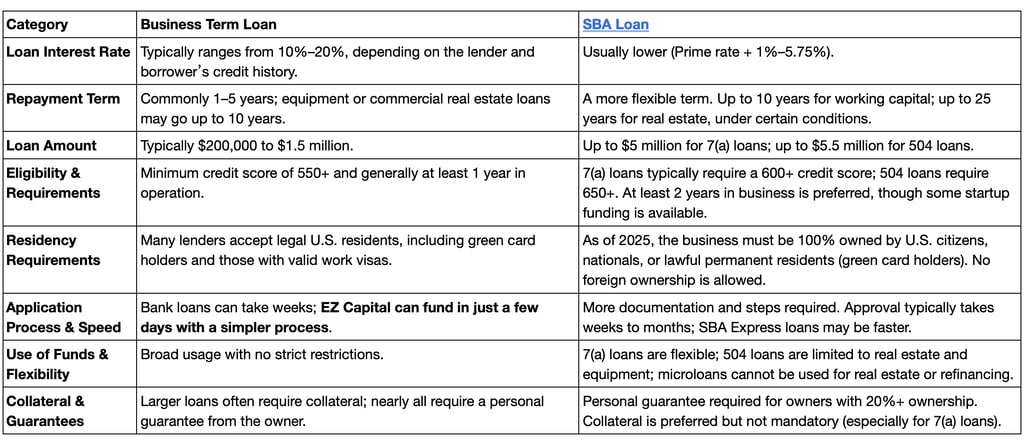

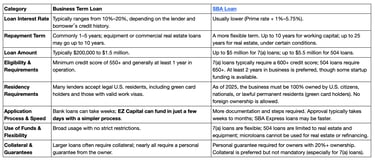

5.Term Loan vs. SBA Loan: Which One to Choose?

Business term loans are a foundational financing tool for U.S. small businesses, offering a balance of flexibility, affordability, and structure and providing a clear path to funding. By understanding how term loans work—their pros and cons, types, eligibility requirements, uses, and how they compare to SBA loans—you can make well-informed decisions for your company’s growth.

At EZ Capital, we specialize in delivering intelligent, customized financing solutions for small business owners. Through our platform, you can compare multiple loan offers and find one that best fits your financial profile. Most of our term loan products allow for early repayment with no penalties, helping you reduce borrowing costs and manage cash flow more efficiently.

If you’re exploring funding options or still have questions about how to apply, we’re here to help. You can call (929) 230-1888 or use the application form. Our experienced team will guide you with professional, tailored support so you can move forward confidently and affordably.

We wish you successful financing and business growth ahead! 🚀

Conclusion

© EZ Capital 2026. All rights reserved.

Fulfillment Policy | Privacy Policy | Terms and Conditions of Service

EZ Capital is a financial technology company, not a bank. Business financing is provided by EZ Capital and/or its partners.

All applications are subject to approval. Additional fees may apply.

Certain financing products and/or services may not be available in certain states.

Contacts

Sales Hotline

Customer Support

(332) 230- 0606