A Comprehensive Guide to SBA Loans and the Latest Policies

SBA loans are known for their relatively low interest rates, extended repayment terms, and higher approval amounts compared to conventional loans.

ENGLISH

6/23/2025

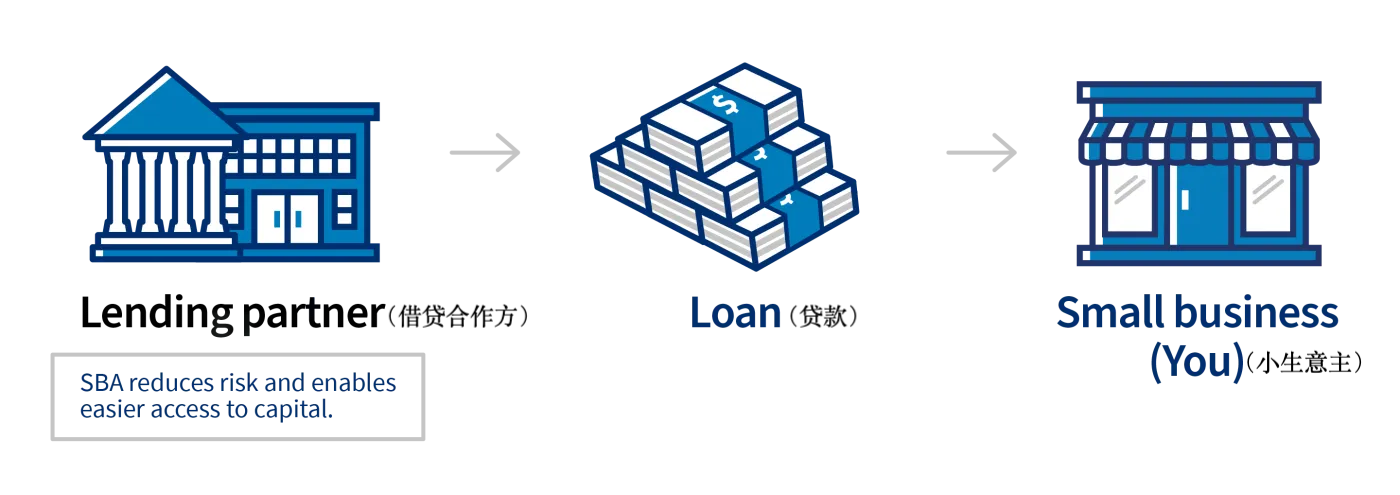

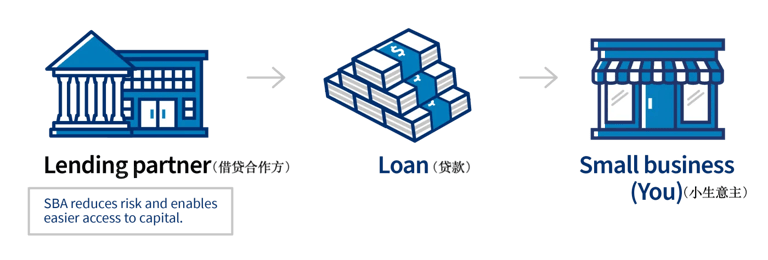

SBA loans have long served as a reliable financing option for small businesses across the United States. During the COVID-19 pandemic, SBA programs such as the Paycheck Protection Program (PPP) and Economic Injury Disaster Loans (EIDL) provided critical financial support to help small enterprises navigate economic challenges. While the Small Business Administration (SBA) does not directly issue these loans, it collaborates with SBA-approved lenders—including banks, credit unions, and other financial institutions—to facilitate the lending process. Through its guarantee of a portion of the loan amount, the SBA reduces the risk for lenders, thereby making it more feasible for small businesses to secure the funding they need.

SBA loans are known for their relatively low interest rates, extended repayment terms, and higher approval amounts compared to conventional loans. While the loan application process may involve more documentation and the loan approval process may take some time, the benefits often outweigh the complexities. This article delves into the specifics of SBA loans, their advantages, and the eligibility criteria.

1.What is an SBA Loan?

An SBA loan is a business loan partially guaranteed by the U.S. Small Business Administration, designed to provide financing support to small businesses. SBA loans cater to small business owners, including startups and existing businesses, and can be used for various purposes, such as working capital, equipment purchases, real estate acquisition, or business expansion.

It's important to note that the SBA itself typically does not provide loans directly (except in special cases like disaster loans). Instead, small businesses apply through participating banks, credit unions, or other approved financial institutions, with the SBA offering a partial guarantee on the loan.

2.What Are the Advantages of SBA Loans?

The SBA's guarantee reduces the risk for lenders, making them more willing to extend credit to small businesses, thereby increasing the likelihood of loan approval.

Government Guarantee

Versatile Use

Extended Repayment Terms

Competitive Interest Rates

Access to Business Counseling

SBA loans can be utilized for a wide range of business needs, including starting a new business, purchasing equipment, expanding operations, hiring employees, acquiring land or facilities, and providing working capital.

Interest rates for SBA loans are typically lower than those of conventional loans.Rates are often based on the Prime Rate plus a fixed spread, which varies depending on the loan amount and term.For example, as of June 2025, SBA 7(a) loan rates range from 9.75% to 12.25%, depending on the loan size and whether the rate is fixed or variable.

Compared to many traditional loans, SBA loans offer longer repayment periods. For instance, working capital loans can have terms up to 10 years, while loans for real estate purchases can extend up to 25 years. This results in lower monthly payments, easing cash flow pressures on businesses.

Borrowers of SBA loans may also receive additional support, such as free business counseling or guidance services provided by SBA partners, to help manage and grow their businesses effectively. Additionally, successfully obtaining an SBA loan can enhance your business's credit profile and strengthen relationships with banks, facilitating future financing opportunities.

3.What Types of SBA Loans are Available?

The SBA offers various loan programs to meet different business needs, including 7(a) Loan Program, the 504 Loan Program, the Microloan Program, SBA Express, SBA Export Express loans, and SBA disaster loans, etc. The most common types include the 7(a), 504 and the microloan. Each serves specific purposes and caters to different business sizes.

(1) SBA 7(a) Loan

(2) SBA 504 Loan

(3) SBA Microloan

The 504 Loan Program is designed for financing large fixed asset purchases and long-term investments, such as buying commercial real estate (e.g., office buildings, warehouses), constructing or renovating facilities, or acquiring substantial machinery and equipment.

Maximum Loan Amount: Typically, a 504 loan involves a partnership between a Certified Development Company (CDC) and a bank. The SBA-backed CDC portion can cover up to 40% of the project cost (up to $5.5 million for certain projects), the bank provides 50%, and the borrower contributes a minimum of 10% as a down payment.

Repayment Terms: Depending on the project and asset type, terms can be 10, 20, or 25 years.

Interest Rates: The CDC portion typically has a fixed interest rate tied to U.S. Treasury rates, often resulting in favorable terms.

Eligibility Requirements: Applicants must meet SBA size standards and use the loan strictly for approved purposes (e.g., purchasing fixed assets). If the loan is for real estate, the business must occupy at least 51% of the property. Generally, borrowers should have a good credit history and be able to provide some form of collateral.

Overall, if your business plans involve acquiring or upgrading real estate or equipment and you seek long-term, fixed-rate financing, the 504 loan is an appropriate choice.

The 7(a) Loan Program is the SBA's primary and most flexible loan option, suitable for a wide range of business financing needs. Common uses include providing working capital, purchasing equipment or inventory, expanding operations, acquiring existing businesses, or buying commercial real estate.

Maximum Loan Amount: Up to $5 million.

Repayment Terms:

Working capital: up to 10 years.

Equipment purchases: up to 10 years.

Real estate purchases: up to 25 years.

Interest Rates: Rates are subject to SBA maximums and are typically based on the Prime Rate plus a spread. As of June 2025, fixed rates for SBA 7(a) loans range from 9.75% to 12.25%, depending on the loan size.

Eligibility Requirements: Applicants should have a good credit history and a viable business plan or operational record.

In summary, if you operate a well-managed small business and require substantial funding for various purposes, the 7(a) loan is often the preferred option.

The Microloan Program offers small, short-term loans to small businesses or certain non-profit childcare centers. It's ideal for businesses needing less capital, such as purchasing inventory, supplies, small equipment, or as startup capital. Microloans cannot be used to pay existing debts or purchase real estate.

Maximum Loan Amount: Up to $50,000, with the average loan around $13,000.

Repayment Terms: Maximum term of 6 years.

Interest Rates: Determined by intermediary lenders; typically range from 8% to 13%, reflecting the higher risk and smaller loan amounts.

Eligibility Requirements: Microloans are more accessible to startups or businesses with limited credit history.Applicants usually need to provide a sound business plan and demonstrate the ability to repay the loan.

In summary, if you're a small business or startup requiring a modest amount of capital and lack extensive operational history or credit records, a microloan is an ideal option. The application process is generally simpler and faster than for larger SBA loans, though specific requirements vary by lender.

4.What Are the Eligibility Criteria for SBA Loans?

Business Size and Type

Must be a for-profit business operating in the U.S. and meet SBA size standards.

Operational History

Ownership

Credit-worthiness

While specific requirements vary by loan type and lender, general SBA loan eligibility requirements include:

If not a startup, the operating business should have at least two years of stable financial records or revenue history.

As of 2025, businesses must be 100% owned by U.S. citizens or lawful permanent residents (green card holders). Any form of foreign ownership, including minority stakes, is no longer permitted.

Applicants should have a good credit score and no outstanding federal debts. Generally, a minimum credit score of 650 is recommended.

5.What If You Encounter Difficulties Applying for an SBA Loan?

Securing an SBA loan can provide business owners with the necessary capital to grow or expand their enterprises. However, applying for an SBA loan is a significant financial decision that requires careful consideration. Applicants must submit all required documentation to complete the application process and utilize the funds in accordance with the loan agreement.

It's worth noting that the documentation required for an SBA loan is only slightly more extensive than that for traditional financing options. If you have funding needs but are uncertain about the eligibility criteria or the application process for an SBA loan, we invite you to contact the EZ Capital team. We are committed to providing you with professional and customized services, offering practical advice to help you achieve entrepreneurial success with minimal financial cost.

© EZ Capital 2026. All rights reserved.

Fulfillment Policy | Privacy Policy | Terms and Conditions of Service

EZ Capital is a financial technology company, not a bank. Business financing is provided by EZ Capital and/or its partners.

All applications are subject to approval. Additional fees may apply.

Certain financing products and/or services may not be available in certain states.

Contacts

Sales Hotline

Customer Support

(332) 230- 0606