Low Credit? Fast-Funding Merchant Cash Advances (MCA) Can Help!

A Merchant Cash Advance (MCA) could be a more practical, more flexible financing solution. It focuses on your daily business revenue, not your credit score or collateral.

ENGLISH

7/24/20256 min read

Imagine this: you run a small restaurant and want to upgrade your outdoor seating before the summer rush. You apply for a business loan from the bank, only to be rejected since your business is too new, your immigration status is limited, and your credit score isn’t ideal. In times like these, is there a more flexible, internal way to meet your cash flow needs?

A Merchant Cash Advance (MCA) could be a more practical, more flexible financing solution. It focuses on your daily business revenue, not your credit score or collateral. Many MCA providers accept applications from EAD (work permit) holders, approve applicants with credit scores as low as 450, and don’t require collateral. For small businesses that struggle to qualify for traditional bank loans, merchant cash advances offer quick access to usable working capital. The application process is simple, funding is fast, and repayment schedules are flexible—either based on a percentage of sales or through fixed daily or weekly deductions.

In this article, we’ll walk you through how merchant cash advances work, what their terms look like, when and how they’re used, and help you decide whether it’s the right business financing tool for your business.

1. What Is a MCA and How Does It Work?

According to a Federal Reserve survey, merchant cash advances have an approval rate of around 90%, much higher than traditional small business loans, which average about 66%.

A Merchant Cash Advance (MCA) is a unique type of revenue-based financing tailored to small businesses. The MCA provider gives the business owner a lump-sum advance of cash, which is then repaid based on future business sales. MCA uses fixed factor rates instead of a traditional interest rates and allows flexible repayments options—either as a percentage of daily debit card/credit card sales or as fixed daily/weekly deductions. This makes MCAs ideal for industries like restaurants with variable cash flow.

Most merchant cash advance companies integrate directly with the merchant’s payment processor to track daily revenue and automatically deduct repayments. This eliminates the need for complex credit underwriting or asset-based collateral, significantly speeding up the approval and funding process. For businesses with strong credit card sales but weaker credit histories—or those shut out of traditional financing—MCA offers a fast and efficient alternative.

2. Key MCA Terms

Advance Amount: The lump-sum advance usually ranges from several thousand to several hundred thousand dollars. It typically does not exceed 1 to 2.5 times the merchant’s average monthly revenue. The exact maximum varies by provider and underwriting result.

Factor Rates: MCAs don’t use traditional interest rates. Instead, a factor rate (typically 1.1–1.2) is used to calculate the repayment total. For example, a $10,000 advance with a 1.2 factor rate would require a total repayment of $12,000.

Repayment Method: If using percentage-based repayment, the MCA provider collects a fixed percentage (called a holdback rate, typically 5%–20%) of daily sales. If using fixed repayment, the MCA provider deducts a fixed dollar amount daily or weekly from your business bank accounts, regardless of sales performance.

(See Section 3 for detailed examples.)Repayment Frequency: MCA repayments are frequent and automated. The most common frequencies are daily, weekly, or biweekly. Some merchant cash advance companies allow monthly payments.

Repayment Term: MCA terms are typically under one year. The exact duration depends on your daily debit card/credit card sales and the agreed-upon deduction rate.

Collateral and Guarantees: Most MCAs do not require any physical collateral or personal guarantees. The provider relies on your business’s future sales as repayment security.

💡 With EZ Capital, early repayment may qualify for exclusive discounts—pay faster, save more!

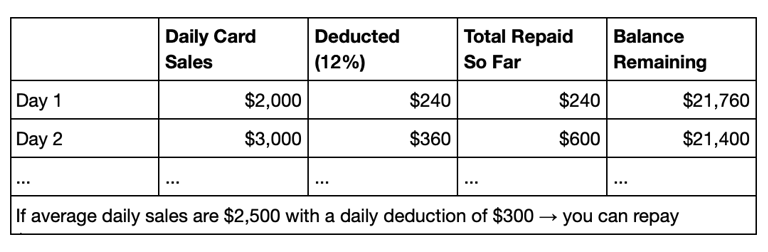

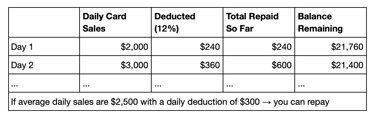

3.MCA Repayment Structures

3.1 Revenue-Based Repayment

The MCA provider deducts a fixed percentage of your daily credit/debit card sales until the advance and fees are fully repaid. The more you sell, the faster you repay.

📌 Not sure how that works? Here’s a simple example (for illustration only—fees and totals may vary):

Advance: $20,000

Factor Rate: 1.1 → Total Repayment = $22,000

Holdback Rate: 12% → 12% of daily card sales automatically deducted

Repayment Example:

✅ Repayment fluctuates with revenue—higher on busy days, lower in slow periods. Cash flow stays manageable.

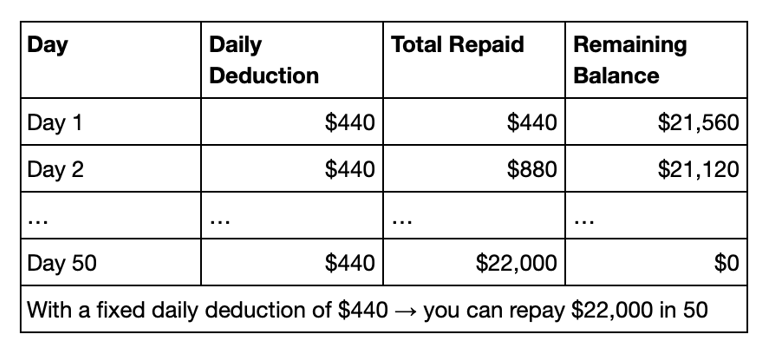

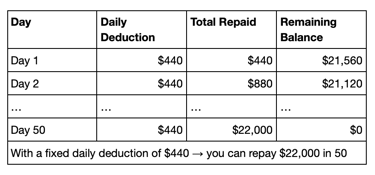

3.2 Fixed Amount Repayment

Another repayment structure involves setting a fixed deduction amount from business bank accounts regardless of sales volumes on a daily or weekly basis. The fixed amount is estimated based on the merchant’s average monthly revenue and remains consistent throughout the repayment period.

📌 Example (illustrative only—excluding any fees):

Advance: $20,000

Factor Rate: 1.1 → Total Repayment = $22,000

Repayment: Fixed ACH deduction of $440/day

Repayment Example:

✅ Predictable and easy to budget for, though fixed payments may feel tighter in slower months.

4.What Types of Businesses Are a Good Fit for MCA?

Businesses with high credit card volume:

Ideal for merchants processing $5,000+ per month in debit/credit card sales.

Newer or credit-challenged businesses:

If you’ve been operating for a short time or have poor credit reports but steady income, MCA is often still an option.

Seasonal businesses:

Merchant cash advance repayment aligns with fluctuating revenue, making it ideal for seasonal retail businesses, restaurants, and tourism businesses.

Asset-light service providers:

Service-based or online businesses without hard assets for collateral can still qualify for MCA.

Businesses needing short-term working capital:

Perfect for urgent needs like restocking, repairs, renovations, or time-sensitive opportunities.

5.MCA Eligibility Requirements

To qualify for most merchant cash advances programs, businesses generally need:

Credit Card Payment Activity: You must accept credit cards and have a consistent transaction history.

Minimum Monthly Revenue: Typically at least $5,000/month in debit/credit card sales.

Time in Business: Most providers require at least 5 months of operation with steady revenue.

Immigration Status: Merchant cash advance is accessible to applicants with EAD cards, green cards, or U.S. citizenship.

Credit Inquiry: Merchant cash advance providers accept lower FICO scores—some as low as 450. Higher credit scores may secure better terms, but even businesses with relatively poor business credit history can often qualify.

6.Pros and Cons of MCA

✅ Advantages

Fast Approval: MCA application requirements generally focus on your revenue info, not an extensive credit report. Simple applications with minimal paperwork. Funding in 24–48 hours from merchant cash advance companies is common.

Soft Qualifications: Credit requirements and time in business requirements are much softer than traditional loans.

No Collateral Needed: Most MCA providers don’t require physical assets or personal guarantees.

Various Use of Funds: Use the money for any business purpose—restocking, payroll, repairs, marketing, etc.

Early Repayment Discounts: With EZ Capital, repaying early may unlock exclusive fee discounts and more flexible terms. Contact us to learn more!

❌ Disadvantages

Frequent Repayments: MCA repayments occur daily/weekly, which can create pressure on cash flow during slow periods.

Higher Total Costs and Risks: Compared to traditional loans, MCA costs are generally higher, both in total dollars and equivalent APR.

No Credit Building: Most MCA providers do not report repayment to credit bureaus, so it won’t help build your business or personal credit score.

7.Conclusions

A Merchant Cash Advance is essentially a way to “leverage your future sales to fund today’s growth.” Compared to traditional loans, MCA offers faster approvals, lower entry barriers, no collateral requirements, and flexible repayment options. While the cost may be higher, for businesses that need urgent capital and struggle to qualify for bank financing, MCA can be a highly practical and effective funding option.

Still have questions about how MCA works or whether it fits your business needs? Contact the EZ Capital team for a free, personalized consultation. We’ll help you evaluate your options and design a financing plan tailored to your goals.

EZ Capital is a smart business financing platform dedicated to empowering small business owners with tailored lending solutions. We help you compare funding options quickly and confidently—so you can move forward with clarity and momentum.

We wish you great success in funding and growth! 🚀

© EZ Capital 2026. All rights reserved.

Fulfillment Policy | Privacy Policy | Terms and Conditions of Service

EZ Capital is a financial technology company, not a bank. Business financing is provided by EZ Capital and/or its partners.

All applications are subject to approval. Additional fees may apply.

Certain financing products and/or services may not be available in certain states.

Contacts

Sales Hotline

Customer Support

(332) 230- 0606